Taxing the Rich is Not New and It has Never Worked

The Case Against Warren's Wealth Tax

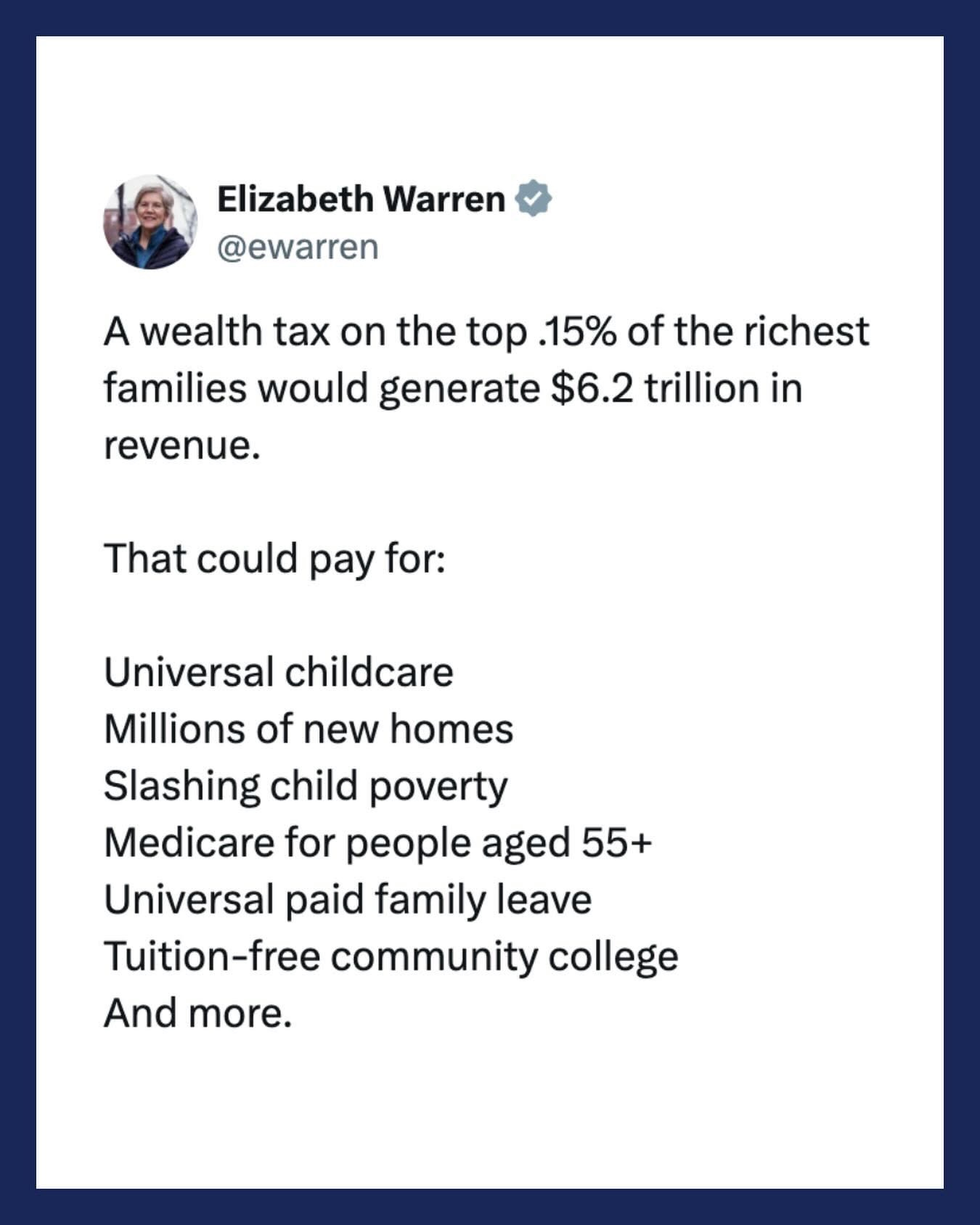

There is a particular kind of political promise that recurs in American life with the reliability of a comet. It appears every generation or so, trailing the same glittering tail of assurances: that a narrow tax on a narrow slice of the wealthiest citizens will, at a stroke, fund the programs we have long wanted and cannot seem to afford. The latest iteration arrived this month in a social media post from Senator Elizabeth Warren. A wealth tax on “the top .15% of the richest families,” she writes, would generate $6.2 trillion in revenue — enough, her graphic promises, to pay for universal childcare, millions of new homes, an expanded child tax credit, Medicare eligibility at 55, universal paid family leave, tuition-free community college, “and more.”

It is an appealing tableau. It is also, in every meaningful particular, a proposition that history has already tested and found wanting. What is being offered as bold and novel is in fact among the most thoroughly attempted policies of the last half-century, and its record is not a matter of ideological dispute. It is a matter of public record, compiled by governments of the left and the right, in wealthy countries and poor ones, and it points uniformly in a single direction.

Before turning to that record, it is worth examining the arithmetic on its own terms.

The Arithmetic Does Not Work

The first clarification the tweet declines to offer is that its $6.2 trillion figure is not annual revenue. It is a ten-year projection from Emmanuel Saez and Gabriel Zucman, the Berkeley economists who designed Warren’s proposal. Divided by ten, it implies something closer to $620 billion per year — and that is the ceiling, not the floor, of the estimate.

Independent analysts have been considerably less sanguine. The Penn Wharton Budget Model, widely regarded as the most rigorous non-partisan fiscal scorekeeper in Washington, projected that the 2021 version of Warren’s bill would raise roughly $2.1 trillion over a decade, or about one-third of the Saez-Zucman figure. Lawrence Summers, the former Treasury Secretary and no adversary of progressive taxation, co-authored a widely circulated critique arguing that the Saez-Zucman estimate assumes away the practical reality of how the wealthy respond when targeted. The realistic annual yield, in other words, is not $620 billion but something nearer $210 billion.

Set that figure against the spending list. Universal childcare, priced at the scale of President Biden’s American Families Plan, runs approximately $40 billion per year. Universal pre-K adds another $20 billion. Universal paid family leave costs roughly $22 billion. Tuition-free community college, depending on design, consumes $10 to $28 billion. Lowering Medicare eligibility to age 55 — a far larger step than the Congressional Budget Office scored when it estimated a drop to 60 would cost roughly $30 billion annually — would conservatively require $60 to $100 billion each year. A serious housing construction program of the scale implied by “millions of new homes” has been priced by the Biden administration at $100 billion or more per year. Restoring the expanded Child Tax Credit that briefly halved American child poverty in 2021 cost approximately $100 billion annually on its own.

The sum of these conservative estimates lies between $350 and $420 billion each year, before the catch-all “and more” at the bottom of Warren’s list. Even using her own inflated revenue figure, the ledger is tight. Using a credible one, it does not balance at all. And this is to say nothing of the fact that these are permanent programs whose costs will grow with demographics and healthcare inflation, funded notionally by a ten-year revenue window whose yield is almost certain to decline over time as the tax base migrates or restructures.

A Policy With a Long Pedigree and a Short Record

The more consequential problem with Warren’s proposal is not its arithmetic but its pretense of novelty. A wealth tax is not an untried idea awaiting American courage. It is among the most extensively attempted tax instruments in the developed world, and the trajectory of its adoption tells a sobering story.

In 1990, twelve OECD countries levied individual net wealth taxes. By 2017, only four remained. Austria repealed its wealth tax in 1994. Denmark and Germany followed in 1997. The Netherlands abandoned its version in 2001. Finland, Iceland, and Luxembourg all repealed theirs in 2006. Sweden — the social democracy American progressives most frequently cite as a model — eliminated its wealth tax in 2007 under a Social Democratic government. France, the largest economy to have attempted it, repealed its Impôt de Solidarité sur la Fortune in 2018.

The reasons offered by these governments were strikingly uniform across political coalitions and national circumstances: administrative complexity and enforcement costs that, in some cases, significantly reduced net revenue, genuine difficulty assigning value to illiquid assets such as private businesses and fine art, yields that disappointed the projections used to justify the tax in the first place, and, above all, capital flight that produced net fiscal losses once the departed taxpayers’ income, consumption, and capital gains taxes were subtracted from the balance sheet.

France

The most rigorously studied of these experiments is the French one. The economist Eric Pichet, whose analyses are now standard references in the field, estimated that capital flight attributable to the ISF totaled roughly €200 billion between the tax’s reintroduction in 1988 and his 2007 assessment. The tax raised approximately €3.6 billion at its peak. Pichet calculated that it caused an annual fiscal shortfall of about €7 billion — meaning the French state lost nearly twice what the tax collected once the foregone revenue from emigrated taxpayers was accounted for. His estimate of the tax’s drag on annual GDP growth was 0.2%, a figure that compounds into serious economic harm over decades.

At least 10,000 wealthy French citizens left the country primarily to avoid the tax. Many settled in Belgium, whose shared language and proximity made relocation trivial. Among those departed were members of the Taittinger champagne dynasty, whose patriarch publicly attributed the sale of his family’s storied house to the tax. When President Macron terminated the ISF in 2017, the move was broadly understood as the belated acknowledgment of a generation-long policy failure.

Sweden

The Swedish case is instructive precisely because Sweden occupies such a central place in the American progressive imagination. Its wealth tax drove out several of its most celebrated entrepreneurs. Ingvar Kamprad, the founder of IKEA, relocated to Switzerland. The Rausing family, owners of the packaging giant Tetra Pak, departed for the United Kingdom and Switzerland. By the time a Social Democratic government repealed the tax in 2007, the consensus across the Swedish political spectrum was that the revenue it generated did not justify the capital outflow it produced. The widely admired economic renewal Sweden has enjoyed in the years since began after this repeal, not before it.

Norway

Norway offers an unusual opportunity: it is among the few European countries that still levies a net wealth tax, and it is producing a real-time demonstration of why most of its neighbors do not. After the Norwegian center-left government raised the top wealth tax rate to 1.1% in late 2022, more than thirty Norwegian billionaires and multimillionaires emigrated during 2022 alone — more than had left in the preceding thirteen years combined. By the end of 2023, at least 82 wealthy Norwegians with a combined net worth of approximately $4.3 billion had relocated, the substantial majority to Switzerland. The departure of a single industrialist, Kjell Inge Røkke, was estimated to cost the Norwegian treasury roughly $16 million per year on its own.

The Norwegian experience has surfaced a mechanism that theoretical models often miss: because the wealth tax applies to the unrealized value of privately held companies, business owners are compelled to extract dividends from their firms simply to pay the tax. The result is a tax that functionally penalizes the ownership of productive, reinvested capital — the very capital that generates jobs and future growth.

India

India levied a wealth tax for fifty-eight years before abolishing it in 2015. The rationale offered by Finance Minister Arun Jaitley was unusually direct for a government official: “The practical experience has been it’s a high cost and a low yield tax.” The administrative apparatus required to value diverse assets across a vast country consumed most of what the tax produced.

The American Cautionary Tale

The familiar American counterpoint to this evidence is that the United States once imposed top marginal income tax rates of 70%, 80%, and even 91% during the postwar boom, and the republic flourished. The rates existed; the payments did not. The tax code of that era was constructed as much to generate avoidance opportunities as to collect revenue, and the effective rates borne by high earners were a small fraction of the nominal ones.

The evidence for this lies in the receipts themselves. When the top marginal rate stood at 91%, the top half percent of earners paid approximately 14 to 15 percent of all federal income taxes. By the late 1990s, after the top rate had been reduced to 39.6%, the top half percent was paying nearly 30 percent. Lower headline rates applied to a broader base produced a more progressive distribution of the federal tax burden, not a less progressive one.

It is equally worth noting that the 1970s — the decade of the highest sustained effective taxation and most intensive regulation in postwar American history — produced stagflation rather than prosperity. The tax reforms of the 1980s coincided with the longest peacetime economic expansion the country had then experienced. One need not be a supply-side partisan to observe that the historical record is not kind to the proposition that aggressive taxation of wealth and capital produces either fiscal bounty or broad-based flourishing.

The Alternative Milton Friedman Proposed

Milton Friedman spent much of his career articulating why progressive income taxation, let alone the confiscation of wealth, was both economically destructive and strategically counterproductive for those genuinely committed to helping the poor. In Capitalism and Freedom, published in 1962, he laid out an alternative whose contours have aged remarkably well.

Friedman’s proposal had two elements. The first was a flat tax applied to income above a generous personal exemption — a single rate, few deductions, administered simply. The second was the negative income tax: a direct cash transfer to households whose incomes fell below the exemption threshold, phased down gradually as earnings rose so that work always paid more than idleness. The combined system would replace the tangled apparatus of food stamps, housing vouchers, energy subsidies, childcare credits, and the rest — what Friedman memorably described as requiring “armies of bureaucrats” to administer. If the fundamental problem facing the poor, he reasoned, is that they have too little money, the most efficient remedy is to give them some.

What makes the Friedman framework enduring is that it accomplishes the redistributive objective that progressives claim to seek while avoiding the pathologies that have undone every wealth tax enacted in the modern era. It does not punish the accumulation of productive capital. It does not require states to assign values to illiquid private holdings. It does not drive capital across borders. And it treats its beneficiaries as capable adults rather than as wards of a bureaucracy that determines which specific goods they may purchase with which specific coupons.

Friedman’s negative income tax is the intellectual parent of the Earned Income Tax Credit, which economists across the ideological spectrum recognize as the most effective anti-poverty program the United States has ever implemented. It works because it does precisely what Friedman said it should: it delivers cash directly to working families, without an intermediating bureaucracy.

Why This Matters

The case against Warren’s wealth tax is not that the rich do not have enough or that poverty is inevitable. It is that the policy she proposes has been attempted, repeatedly, across wealthy democracies whose demographic and economic conditions resemble our own, and that it has reliably produced less revenue than its architects promised and more economic harm than its opponents feared. The countries that enacted these taxes have, in the majority, repealed them — not because their political cultures shifted rightward but because the fiscal and economic evidence became impossible to ignore.

Governments of the center-left have repealed wealth taxes alongside governments of the center-right, because the constituencies those taxes were meant to help — working families, the poor, the users of public services — turned out to be worse off once the taxed capital had migrated elsewhere.

There are serious ways to fund the programs Warren describes, if that is the genuine objective. A broader consumption tax paired with generous cash transfers, a simplified income tax with a large exemption, an expanded and enhanced Earned Income Tax Credit, a value-added tax of the kind that finances the European welfare states Warren admires — each of these has a demonstrable track record of producing sustained revenue without driving its tax base abroad (although I do not endorse any of them wholesale). None of them will produce a graphic as satisfying as “tax the .15%.” All of them have a better chance of delivering the outcomes Warren claims to want.

The test of a tax policy is not how it performs on social media in its first week. The test is how it performs in the treasury five years on, after the wealthy have had time to retain counsel, restructure holdings, and, in some cases, relocate. By that standard, the wealth tax has already been tested — twelve times over, across three decades, in economies ranging from the prosperous to the struggling — and its report card is available for anyone willing to read it.

The question before the country is not whether to run the experiment. The question is whether to run it for the thirteenth time, having ignored the first twelve.